Energy auctions can pick winners – and create losers. Will the UK’s next energy auction boost the UK’s lead in tidal energy – or gift our early-mover advantage to competitors overseas? (And of course, we have been here before…)

Well, that didn’t go so well did it?

The recent news from the National Audit Office confirmed what energy insiders have known since last September – the policy team at BEIS got it wrong in the last CfD round.

The report reveals that the £74.50 strike price awarded to Triton Knoll offshore wind farm, owned by the German energy giant Innogy, was far higher than the £57.50 awarded to two wind projects due to start just a year later – with the price dragged upwards by the more expensive energy-from-waste projects that had bid into the same delivery year.

In what was described by BEIS as ‘suboptimal,’ the long-term cost to the consumer will be an estimated £1.5 billion over the contract’s life.

Of course, it is easy to be clever in hindsight – but energy auctions are hard to get right and (as I’ll show shortly), we have been here before.

When introduced, Contracts for Difference were supposed to herald a new market-led framework, where the cheapest technology wins, costs are driven down, the consumer is protected, and government stays well clear of ‘picking winners’.

If we look at offshore wind this is clearly true. The auction system (Triton Knoll aside) has been phenomenally successful in delivering ever-cheaper offshore wind.

But let’s not pretend the government has not picked a winner.

In the same way the government gave a bespoke deal to Hinkley Point C (a supposedly mature technology), and continues to exclude onshore wind (clearly the cheapest) from the auctions process, they supported offshore wind because it was politically easy and played to the UK’s industrial strengths.

It’s clear the energy auctions process does pick winners, and by giving new and maturing technologies a clear route to market costs come down and UK plc stands to gain.

The tide is turning

Which makes it a shame that BEIS has thus far not been minded to offer any support to the UK’s tidal sector in the next auction round.

It is something clearly within their gift.

When the CFD regime was first introduced, DECC (as was) introduced a 100MW ‘minima’ for wave and tidal energy projects in Round 1 – effectively offering a ring-fenced pot for a new technology which clearly could not compete against more mature renewables.

Although (as we all now know), wave energy was further from the market than the PR suggested, tidal energy has made massive strides – not least the MeyGen project in the Pentland Firth which has now exported more than 7GWh to the grid.

Tidal energy could be a massive success story for the UK – it is an area where we have a clear industrial lead, there is global potential, and tidal schemes have a very high UK supply chain content – just the kind of sector the UK’s Industrial Strategy wishes to foster.

We all know that costs will come down as deployment goes up, but the technology does need a route to market – which can be delivered by the clear signal of a tidal energy minima in the next auction round.

Sadly (for Britain), other countries – namely France and Canada – also see the opportunity offered by tidal energy and are lining up to offer deals and incentives to foster the industry’s growth. Atlantis suggest that tidal development in the Raz Blanchard, Normany could create 10,000 jobs and bring €3 billion CAPEX by 2025.

So today we have a scenario where we have spent £millions on building an industrial lead in a potentially global sector, where there are competitor nations, and which now needs an incentive to commercialise.

We couldn’t blow it, surely?

Well, we have before, and I think we could today.

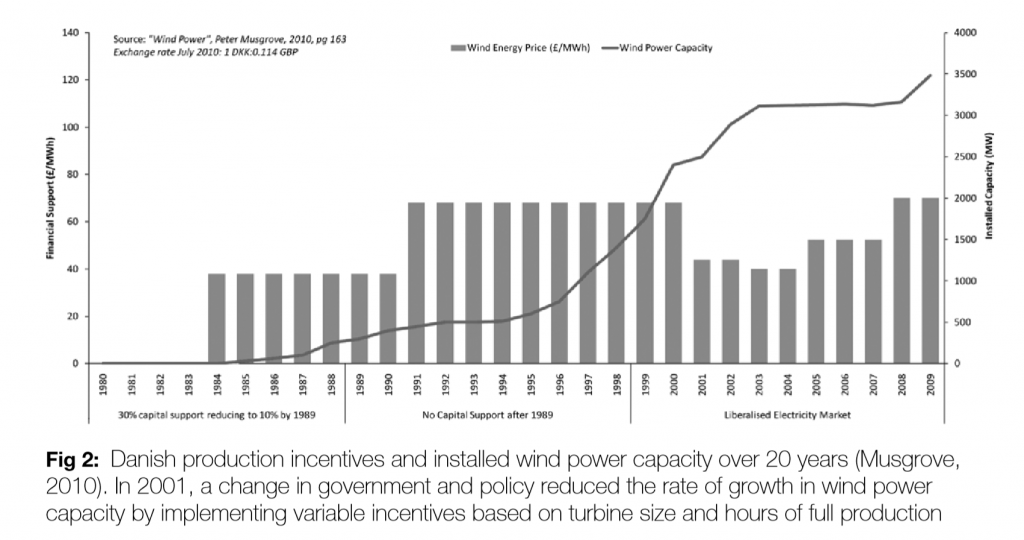

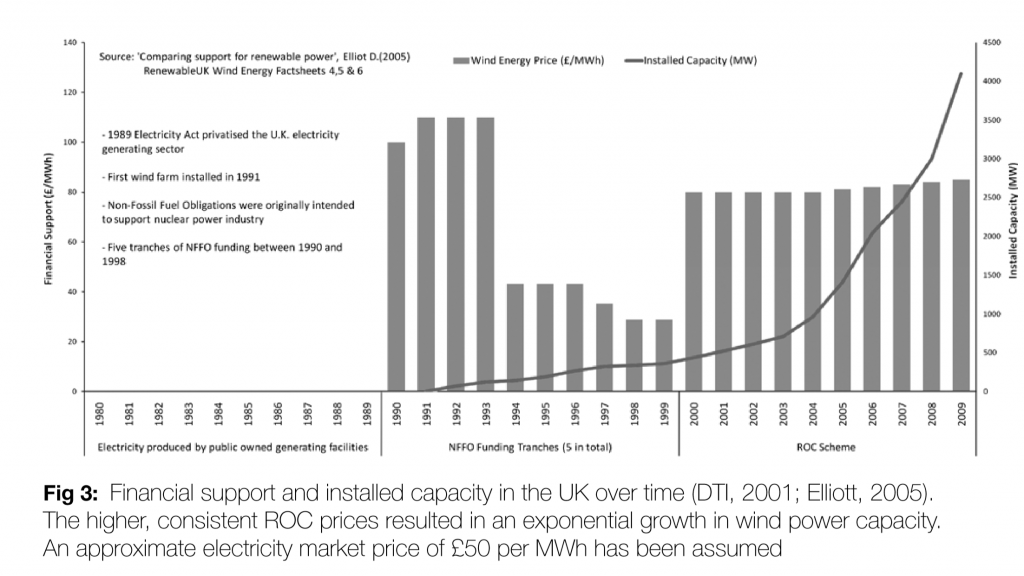

Onshore wind – how we gifted it all to Denmark

In the 1980s – as this paper shows – the UK and Denmark had spent a comparable amount of R&D on onshore wind – a new technology with global potential.

But whilst Denmark incentivised early projects with grid access, and mandated utilities to install wind, the UK brought in a decade of stop-start policies including the Non-Fossil Fuel Obligation (NFFO) – an auctions system which drove down the price of early wind and incentivised developers to import technology and underbid on projects which were subsequently not built.

Consequently, Denmark deployed earlier and faster, and secured first-mover advantage that could easily have been ours.

The net result?

Well, I think you know that. Both countries have plenty of onshore wind projects, but which one has a £multi-billion wind turbine export industry…?

So, the lesson of history is that auction systems can pick winners – but they can also create losers.

Triton Knoll aside, the UK Government has made a fair job of implementing an auctions system that can work – as long as they give your particular technology the nod it requires.

BEIS has already given offshore wind a massive boost. They now need to step up and offer some support for tidal.